Airbus reported record EBIT of 7.1 billion. On a reported basis, the commercial aircraft business that generates nearly 72% of revenue earned less than it did a year ago.

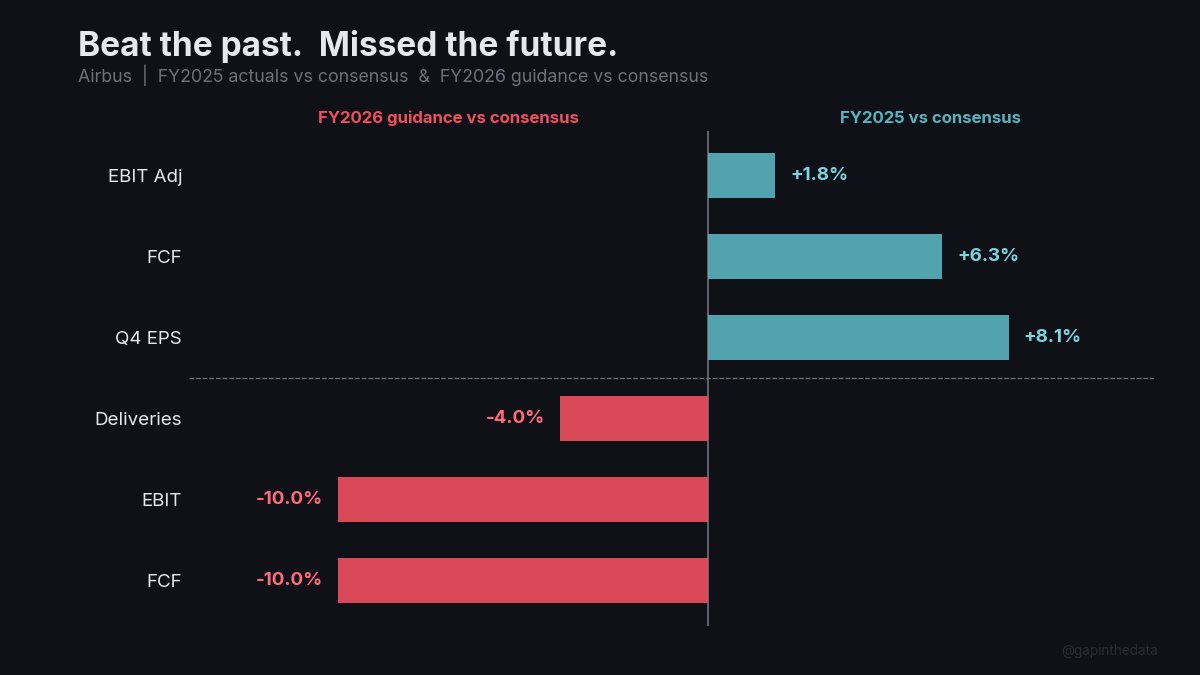

Airbus reported full-year 2025 results this morning from Toulouse. Revenue hit 73.4 billion, EBIT Adjusted rose 33% to 7,128 million and the backlog grew to 8,754 aircraft.1 Guillaume Faury called 2025 “a landmark year”2, and yet the stock fell as much as 7.9%.3 The composition of the +33% explains both the beat and the miss.

I. The Composition of +33%

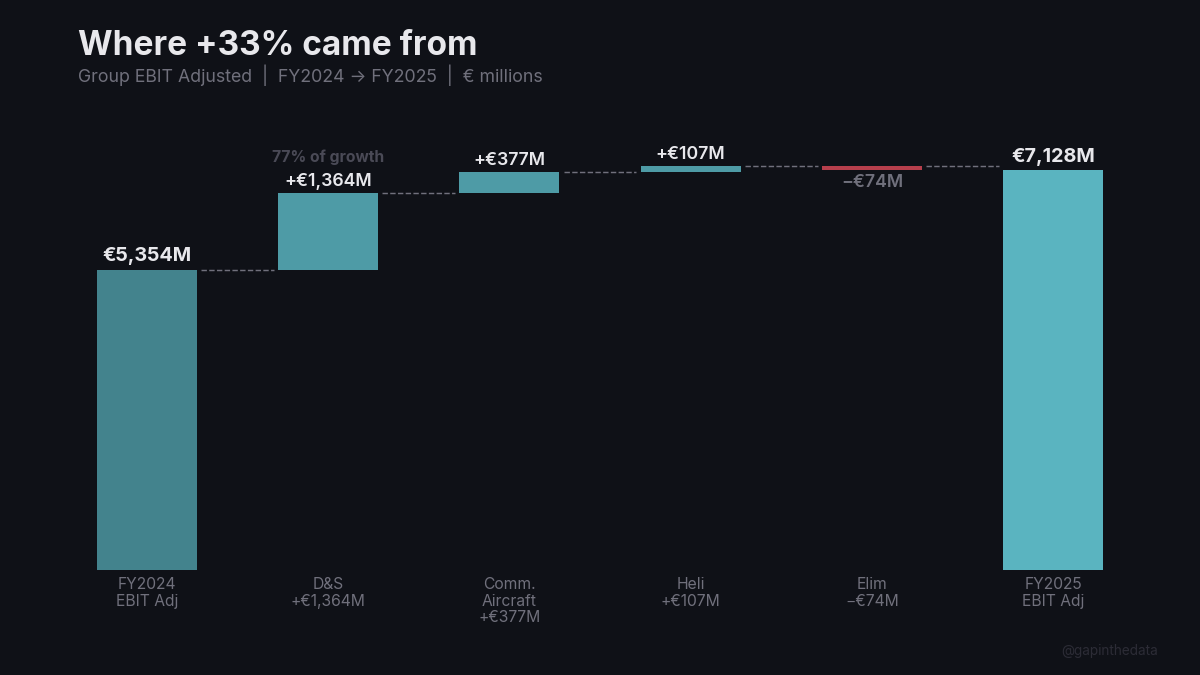

EBIT Adjusted of 7,128 million represented an increase of 1,774 million over FY2024’s 5,354 million.4 Defence & Space swung from a 566 million loss to 798 million in profit (+77%)5, Commercial Aircraft added 377 million (+21%), and Helicopters gained 6%.6 Without Defence & Space, EBIT Adjusted grew approximately 7%.6

Not because D&S had a spectacular year, but because D&S had a catastrophic 2024. 1.3 billion in space-systems charges turned a division that normally earns hundreds of millions into one that lost 566 million.7 The +15% growth in EBIT Reported is against the same depressed base: the D&S reported swing alone (1,295 million) exceeds the entire group reported increase of 778 million.8

II. What the Commercial Aircraft Business Actually Earned

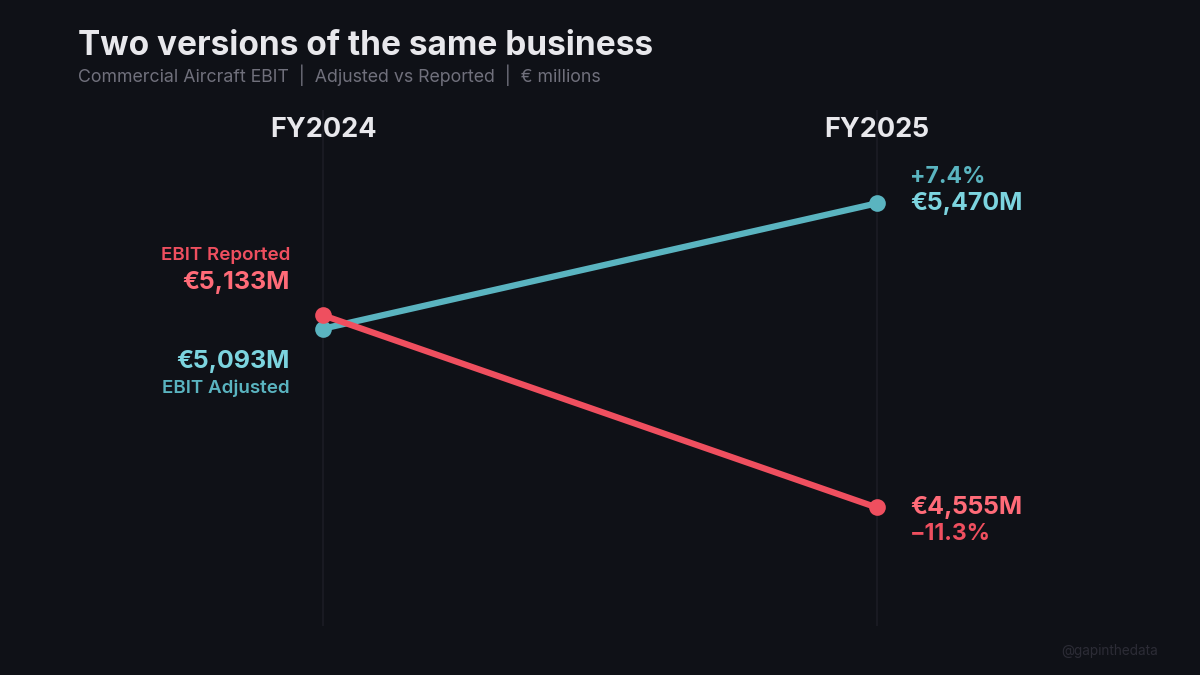

Commercial aircraft is 72% of Airbus’s revenue.9 On an adjusted basis, divisional EBIT rose 7.4% to 5,470 million.10 On a reported basis, it fell 11.3%, from 5,133 million to 4,555 million.11 Per-aircraft reported EBIT fell 14% despite 27 more deliveries.12

CFO Thomas Toepfer: the margin is “not particularly affected, on a per-aircraft basis."13 He was referring to the adjusted number. On that metric, he is correct. On the reported metric, the statement does not hold. Both numbers are in the same filing.

Q4 revenue missed consensus by 5.5%.14 Revenue cannot be adjusted.

III. The Spirit Nesting Doll

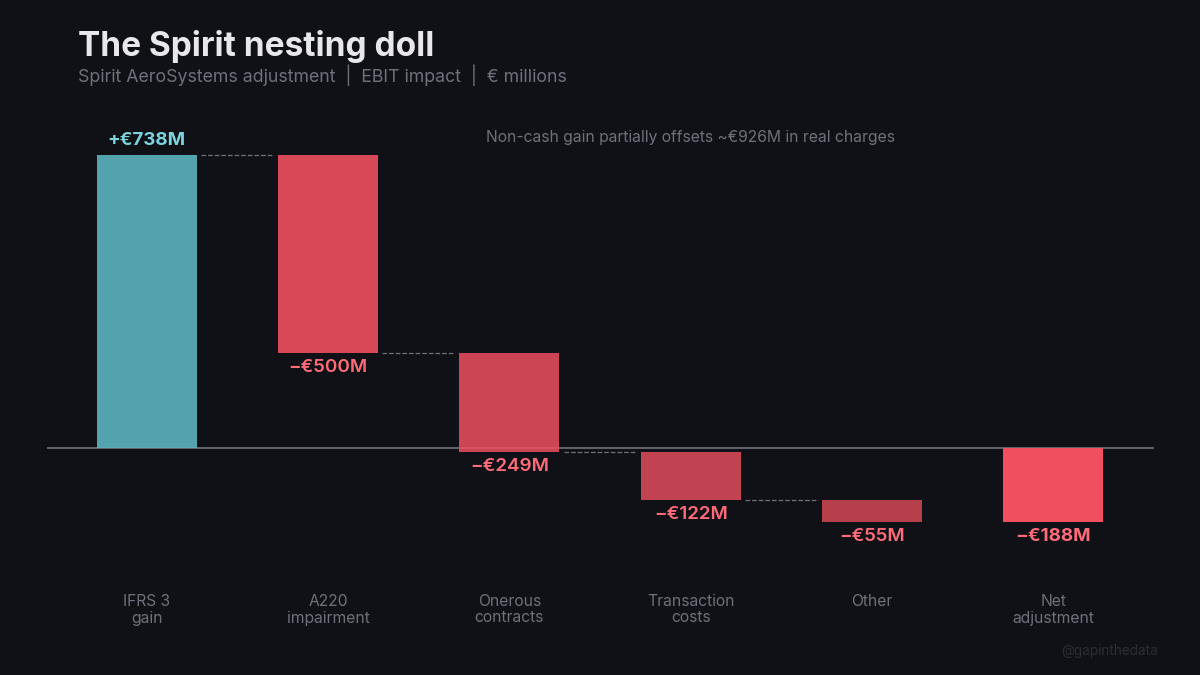

The net Spirit adjustment was negative 188 million, but the 188 million masks components moving in opposite directions.15 A 738 million non-cash IFRS 3 gain partially offset approximately 926 million in real charges: a 500 million A220 impairment, 249 million in onerous-contract provisions, 122 million in transaction costs, and minor items. Toepfer: the gain “notably includes… the termination of the favorable contractual conditions."16 No cash changed hands. The “gain” is the recognition that Spirit’s old below-market pricing is over. Costs are going up.

Three data points converge on the A220. The 500 million impairment at transaction close.15 Investissement Quebec separately wrote off C$400 million from its A220 stake.17 The rate target has slipped from 14 aircraft per month by 2026 to 13 per month by 2028.18 Faury described a “price-volume discussion that takes place to go to profitability to the program."19 The A220 is the only Airbus program with a single engine source: the Pratt & Whitney PW1500G. Unlike the A320neo, there is no CFM alternative.20 The program that just took a 500 million impairment depends entirely on the supplier that resigned from its delivery commitments.

IV. The Forward Picture

Direct quotes from the CEO of Airbus, at the annual press conference, about one of two engine suppliers for its highest-volume program:

“Pratt & Whitney has resigned from the orders we had placed and they had accepted for the volumes in 2026. We have to base our guidance on what they tell us now they’re willing to commit and deliver."21

“They are not respecting their contractual obligations so we want to enforce our rights."21

“Indeed we have initiated a process according to contractual requirements of disputes."21

Asked what was holding Pratt back: “We are very frustrated that they have decided to reallocate more to the in-service because they miss global capability and to the detriment of Airbus where we think they should do more on increasing capabilities to serve both needs at the same time."22

Asked whether the situation was temporary: “I would not take it as something that is very temporary. It’s pacing at least the beginning of the year and what we think is likely to happen."23

Rate 75 has slipped. The new target is “70 to 75 by the end of 2027, stabilizing at rate 75 thereafter."24 The engine duopoly that constrains Rate 75, and the competing incentives within it, is a separate analysis.

There is a pattern: in FY2024, Airbus guided 800 deliveries and delivered 766; in FY2025, guided 820, revised to approximately 790, delivered 793; now FY2026 targets approximately 870 against a Street above 900.25 Each year the delivery target is revised down or missed, and a named supplier is identified.

The order book value fell from 629 billion to 619 billion, a 2% decline despite a record 8,754-unit backlog.26 The Tianjin dependency is a separate risk on the same backlog.

The proposed dividend of 3.20 per share was presented as a 60% increase, measured against the 2.00 regular component of last year’s payout, not the 3.00 total including the special dividend.29

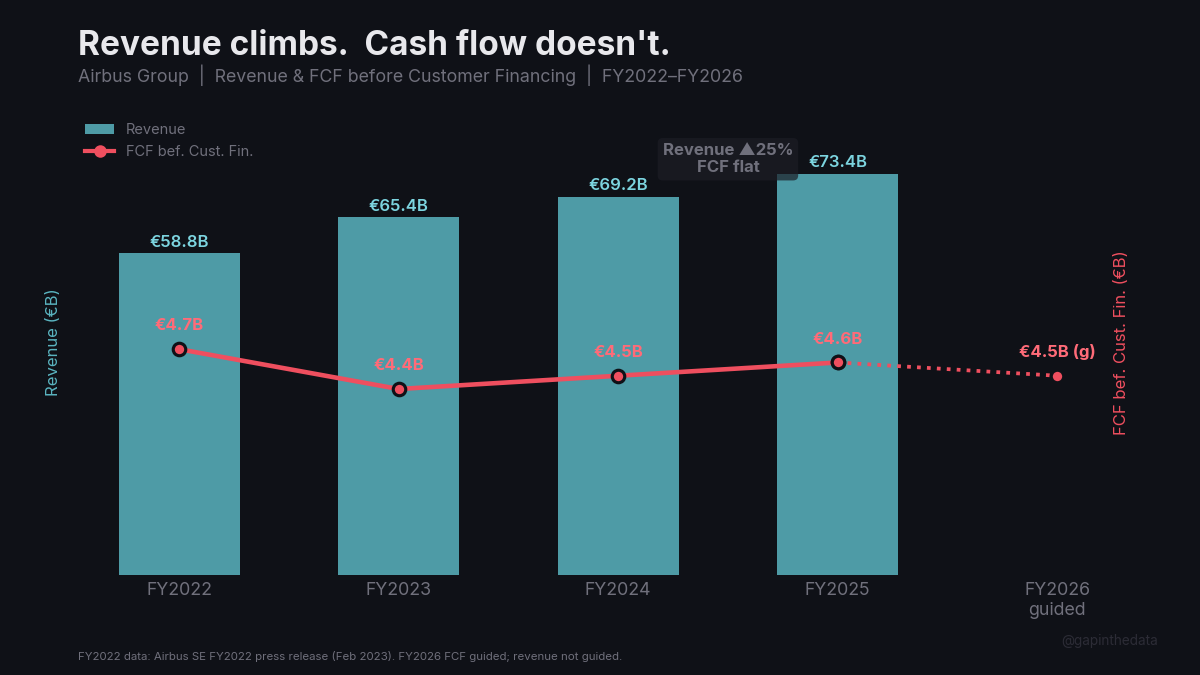

Free cash flow before customer financing: essentially flat for a third consecutive year on 12% revenue growth.27 The 2026 guidance of approximately 4.5 billion would make a fourth.28

Footnotes

1 Airbus SE, “Airbus Reports Full-Year (FY) 2025 Results,” press release, February 19, 2026. EBIT Adjusted 7,128M (+33% vs 5,354M). Revenue 73,420M. Net income 5,221M. Backlog 8,754 aircraft.

2 Airbus Annual Press Conference, transcript, February 19, 2026. Faury: “2025 was indeed a landmark year characterised by very strong demand for our products and services across all businesses.”

3 Market data, February 19, 2026. Airbus (AIR.PA, Euronext Paris) fell from approximately 200 to intraday lows of 185–187. Decline estimates range from 6.2% to 7.9% depending on reference price and timing.

4 Airbus SE press release, “EBIT Adjusted by Segment.” Commercial Aircraft: 5,470M (FY2025) vs 5,093M (FY2024). Helicopters: 925M vs 818M. Defence & Space: 798M vs -566M. Eliminations: -65M vs 9M.

5 Calculation: D&S EBIT Adjusted improvement of 1,364M (from -566M to +798M) / group improvement of 1,774M = 76.9%.

6 Calculation: Group EBIT Adjusted ex-D&S: FY2025 6,330M (7,128M - 798M); FY2024 5,920M (5,354M + 566M). Growth: 6.9%.

7 Airbus SE press release: “FY 2024 had been negatively impacted by 1.3 billion in charges from Space Systems programs.” Toepfer, press conference: “in the financial year ‘24 after the completion of the in-depth technical review of our space programs we’ve recorded a total charge of 1.3 billion.”

8 Airbus SE press release, “EBIT (Reported) by Segment.” D&S reported EBIT swing: from -656M (FY2024) to +639M (FY2025), an improvement of 1,295M. Group EBIT Reported: 6,082M (FY2025) versus 5,304M (FY2024), an increase of 778M.

9 Airbus SE press release. Commercial Aircraft revenue 52,577M / Group revenue 73,420M = 71.6%.

10 Press conference transcript. Toepfer: “the higher commercial aircraft deliveries together with a more favourable hedge rate and lower R&D expenses were partially offset by the impact of tariffs.” The “dollar working capital mismatch & balance sheet revaluation” line in the reconciliation table reflects the difference between the EUR/USD hedge rate embedded in delivery pricing (set years in advance via the hedge book) and the spot rate at which dollar-denominated working capital and balance-sheet items are revalued under IFRS. See Airbus SE press release, KPI Glossary and FY2025 reconciliation detail.

11 Airbus SE press release, “EBIT (Reported) by Segment.” Commercial Aircraft: 4,555M (FY2025) vs 5,133M (FY2024). Change: -11.3%.

12 Calculations: 4,555M / 793 = 5.74M/aircraft (reported); 5,133M / 766 = 6.70M (-14.3%). Adjusted: 5,470M / 793 = 6.90M; 5,093M / 766 = 6.65M (+3.7%). Per-delivery division is a simplification — commercial aircraft EBIT includes aftermarket, services, and engineering support — but the directional finding holds.

13 Thomas Toepfer, CFO, Airbus analyst conference call, February 19, 2026. Referenced in context of per-aircraft margin discussion.

14 Q4 2025 revenue: 25,984M actual versus approximately 27.5B consensus estimate (Visible Alpha, Bloomberg). Miss of approximately 5.5%. Revenue follows IFRS and is not subject to adjustment.

15 Airbus FY2025 financial statements. Spirit AeroSystems adjustment detail: +738M gain from settlement of pre-existing relationship; -500M A220 program asset impairment; -249M onerous contract provisions; -122M transaction costs recorded in other expenses. Additional minor items bring the net to -188M. Facilities acquired: Belfast, Prestwick, Kinston (North Carolina), Saint-Nazaire, Casablanca, and Saint-Eloi, Toulouse. More than 4,000 employees transferred to Airbus and affiliated entities. Boeing completed its acquisition of Spirit AeroSystems on December 8, 2025; Airbus simultaneously took over Spirit’s Airbus-related operations and work packages.

16 Thomas Toepfer, CFO, Airbus analyst conference call, February 19, 2026. Sourced via Yahoo Finance earnings call transcript.

17 Investissement Quebec, A220 program stake write-down of C$400 million, October 2025.

18 Airbus SE press release, Production Ramp-Up Targets. A220: “13 aircraft/month” by 2028. Prior target: 14 aircraft/month by 2026, per Airbus FY2023 and FY2024 guidance updates.

19 Airbus Annual Press Conference, transcript, February 19, 2026. Faury, responding to a question on A220 production trajectory: “We want also to position the product at the right place when it comes to the price and therefore there is a price-volume discussion that takes place to go to profitability to the program.”

20 The A220 is powered exclusively by the Pratt & Whitney PW1500G, a variant of the Geared Turbofan (GTF) family. The A320neo offers a choice between the PW1100G-JM and the CFM International LEAP-1A. The PW1500G is subject to the same powder-metal inspection regime affecting the broader GTF fleet. Source: Airbus program specifications; industry data on GTF fleet inspection requirements.

21 Airbus Annual Press Conference, transcript, February 19, 2026. All three quotes verbatim from Faury. “Pratt & Whitney has resigned from the orders we had placed and they had accepted for the volumes in 2026. We have to base our guidance on what they tell us now they’re willing to commit and deliver.” “They are not respecting their contractual obligations so we want to enforce our rights.” “Indeed we have initiated a process according to contractual requirements of disputes.”

22 Airbus Annual Press Conference, transcript, February 19, 2026. Faury, responding to a question from Ben Katz (Wall Street Journal) on what is keeping Pratt from meeting requirements: “we are very frustrated that they have decided to reallocate more to the in-service because they miss global capability and to the detriment of Airbus where we think they should do more on increasing capabilities to serve both needs at the same time.”

23 Press conference transcript. Faury: “I would not take it as something that is very temporary. It’s pacing at least the beginning of the year and what we think is likely to happen.”

24 Airbus SE press release, Production Ramp-Up Targets. A320 Family: “70–75 aircraft/month” by “End of 2027, stabilising at 75 thereafter.” Previous target: rate 75 by 2027.

25 Airbus reporting. FY2024: guided ~800, delivered 766. FY2025: guided ~820, revised to ~790 (Sofitec panel issue), delivered 793. FY2026: guided ~870 versus consensus ~900–907 deliveries, ~7.5B versus ~8.0–8.3B EBIT Adjusted, ~4.5B versus ~5.0B FCF (consensus compiled from Visible Alpha, UBS, Berenberg, Oddo BHF). At 6.90M per aircraft, 35 fewer deliveries accounts for roughly 240M — less than one-third of the 800M EBIT guidance gap versus consensus.

26 Airbus SE press release. Consolidated order book: 618,824M at 31 December 2025 versus 628,917M at 31 December 2024 (-2%). “Decline reflects weakening of the US dollar and company-wide book-to-bill above 1.” Aircraft backlog: 8,754 units (record).

27 Airbus SE press releases. FCF before Customer Financing: approximately 4.7B (FY2022, per Airbus FY2022 press release, February 2023), approximately 4.4B (FY2023), 4,463M (FY2024), 4,574M (FY2025). Revenue grew from approximately 65.4B (FY2023) to 73.4B (FY2025) — approximately 12%.

28 Airbus SE press release, 2026 Guidance: “Free Cash Flow before Customer Financing of around 4.5 billion.”

29 Airbus SE press release. FY2024 dividend: 2.00 regular + 1.00 special = 3.00 total. Proposed FY2025 dividend: 3.20 per share. The 60% figure compares 3.20 to the 2.00 regular component; the 7% figure compares 3.20 to the 3.00 total payout (including special). See also Airbus FY2025 financial summary: “+6.7%” year-over-year change on total basis.